Daily Commodity Market Analysis -- 06/03/2026

- Clayton Pope

- Jun 3

- 5 min read

Updated: Jun 9

Contract | Close | Net Change |

Corn July '26 | 431 1/2 | -9 |

Corn Dec '26 | 459 3/4 | -6 3/4 |

Beans July '26 | 1154 | -11 1/4 |

Beans Nov '26 | 1167 1/4 | -10 1/2 |

Wheat-Chi July '26 | 687 1/4 | -15 3/4 |

Wheat-KC July '26 | 624 | -10 3/4 |

Wheat-MN July '26 | 626 1/2 | -10 1/2 |

Cotton Dec '26 | 80.51 | -.03 |

Crude Oil July '26 | 96.26 | +2.50 |

US Dollar Index | 99.52 | +0.34 |

Dow Jones | 50688 | -619 |

Outside markets listed may not represent the actual close based on the timing in which this letter was sent.

Daily Glance commodity market

No relief as the sellers remain in control despite some overnight firmness and a higher crude oil market. Our markets all ended near session lows which is an almost 6 month low for July corn, a four month low for July beans, and a six week low for July Chicago wheat.

Selling catalysts include what remains a favorable weather forecast, growing impatience and skepticism regarding China's alleged agreement to step up as a major buyer of our ags, and funds continuing to aggressively shed long positions in corn and soybeans and a willingness to add to wheat shorts.

Outside markets featured stronger crude oil, supported by increased warfare activity and another sharp draw down of the US Strategic Oil Reserve, and weaker stocks for a change.

Key Points/Developments:

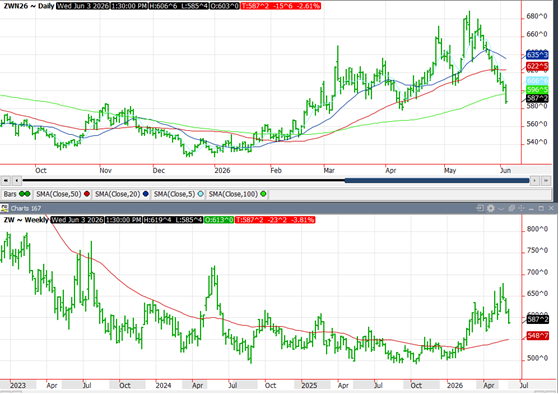

Technicals: The ongoing meltdown in July corn has now left today's settlement only 3 cents above the contract low. That low of 428 1/2 and today's low of 430 are seen as providing some support with more showing up on the weekly chart around 424. Resistance is likely at 440, 452, and the 50 day average near 464.

July soybeans continue to take out recently cited support levels and we now see support right near today's low and close, from 1152-1154 and then below at 1138-1140. Resistance is likely near 1167 and 1188-1190. . Spreads: The July/November carry was little changed today, adding 3/4 cent to end at 13 1/4 as the trade is seemingly not believing any nearby sales to China are likely. We have been saying that we felt the spread would prevent a buying opportunity near a 13-14 cent carry. The July/Dec corn spread widened today by 2 1/4 cents to end at 28 1/4. We certainly find these levels attractive considering the impressive run of exports and possible Chinese interest.

Weather: TStorm left ratings unchanged today, with corn and winter wheat holding at Slightly Favorable and beans at Neutral. Today's forecast summary continues to look crop friendly: Upper-level high pressure leaves a wide area warmer than normal over the next 7 to 10 days -- especially with northward extent. Areas of energy float within the high to generate areas of rain and t-storms over the next 5 days, especially in the eastern Plains, western Corn Belt, and mid-South. A crack in the setup starts Tue.-Fri. (Jun. 9-12) as a large system approaches from the Pacific Northwest with t-storms in the Plains and western Corn Belt, but more-so when a secondary system probably flows by to expand t-storms into a wider area as temperatures at least briefly turn cooler to much cooler starting around 10 days out. The end result is for at least near-normal rainfall for most over the next 14 days, especially with westward extent. |

Markets/Trading Implications

This relentless weakness has been extreme to say the least, with most of the weakness seemingly the result of fund selling. As the charts shown below indicate, this one way action has been virtually non-stop for two weeks. When we refer back to Friday's Commitment of Traders report, which showed activity as of May 26, at which point we had already seen a full week of weakness, in the six sessions since that report date, we have seen July corn drop another 26 cents, July beans another 32 cents, and July Chicago wheat another 48 cents.

This level of selling has undoubtedly slashed the funds' net longs considerably, but our guess is that they are probably still net long something like 100-120k corn contracts and somewhere around 140-150k soybeans, and their net shorts in Chicago wheat could now be as high as 55-60k. (Their reported peak net longs were in the week ended May 5 when they were net long 344k corn and 222k soybeans.)

There has been considerable debate regarding the possibility of the funds' intention to eventually move to net short positions in corn and soybeans, but at this point we see that as unlikely any time soon. There are still many potential positives for these markets, most notably some kind of weather risk premium and the very real possibility that China will in fact finally step up and acknowledge (and act on) the US insistence that they agreed to substantial ag purchases. All of this considered, we suspect there is little additional fund selling in the near future, as the market waits for news on weather, the war, and China's buying intentions.

We find the aggressive selling in wheat the most surprising, considering that wheat fundamentals actually strike us as bullish. Consider these points:-World wheat production by the major exporters is down 35 MMT (almost 8%) from a year ago. -Lowest US wheat acreage since more than 56 years ago. -Smallest projected US wheat production since 1972. -Lowest crop condition rating for this week in 41 years. -US insistence that China has agreed to buy $17 billion of US ag products, not including soybeans, in each of the years 2026-2028.

Because of these facts, we think wheat has extremely little downside, and if/when it can stabilize and recover somewhat, that is likely to lend some support to corn. |

Other Notes

Overnight, Undersecretary of Ag Vaden indicated that China has already begun placing orders for US soybeans as part of their allegedly agreed to commitment. We haven't seen any flash sales confirming this, but if true, those should be coming soon.

Here are the updated daily and weekly corn, soybeans, and wheat charts, along with two crude oil charts.

Static Notes

The Commitment of Traders report for trading through Tuesday, May 26 showed actively traded funds sold a net 88k corn contracts, taking net longs down to 226k contracts. They sold 18k soybeans, bringing net longs down to 190k, and sold 14k Chicago wheat, increasing net shorts to 39k.

In the corresponding week of price activity, July corn lost 18 cents, July beans lost 24 cents, and Chicago wheat lost 32 cents. In the three days since this report, corn lost 8 cents, soybeans were flat, and Chicago wheat lost 26 cents.

Have a nice evening!

Clayton and Taylor

The following table is a "bird's eye" view of our recommended sales levels. Please note that these are meant to be very general guidelines and do not apply to all readers due to the critical differences and unique situations that may exist. Among other possible differences, those current with the following coverage levels might be perfectly comfortable with the expectation of buying some of these sales back at lower levels, whereas others might have no interest in doing so. commodity market

commodity market

Crop Year | 2025/26 | 2026/27 | 2027/28 |

Corn | 80% | 40% | 0% |

Soybeans | 85% | 40% | 0% |

Wheat | 100% | 30% | 0% |

RISK DISCLAIMER:Trading in futures products entails significant risks of loss which must be understood prior to trading and may not be appropriate for all investors. Please contact your account representative for more information on these risks. Past performance of actual trades or strategies cited herein is not necessarily indicative of future performance.

Comments